When Does Manufacturing Matter?

Thinking harder about what we need to build.

Both Democrats and Republicans like to bemoan America’s loss of manufacturing jobs. They agree that Chinese mercantilism poses a threat to American workers and to geopolitical stability. But much of this sentiment rests on memes, slogans, and half-formed ideas. “Manufacturing matters”, “Bring back the good jobs”, and “Rebuild the arsenal of democracy” are vibes, not strategies.

We need to think harder about exactly which manufacturing matters. Specifically:

What does America need to manufacture and why? Nobody argues that the U.S. needs to make T-shirts or socks. Many people believe we should manufacture critical semiconductors and rare earth metals. Some make a strong case for electric motors, drones, and batteries. But what about the thousands of complex manufactured goods in between?

What are America’s specific long-term policy goals? If “economic security”, “military security”, or “developing strategic sectors” is a goal, what exactly do we mean by that? Over the past fifty years, U.S. policymakers have flagged a rotating cast of products and sectors as candidates for federal manufacturing support. Nominees have included semiconductors, telecom infrastructure, HDTV, AI, quantum computing, supersonic transport, wide‑body jets, space launch, satellite manufacturing, shipbuilding, synthetic fuels, solar panels, batteries, nuclear, biopharmaceuticals, advanced chemicals, precision machinery, and robotics.

What are we willing to sacrifice, spend, or trade off to achieve these goals? Achieving anything in the public sector demands exceptional focus. This means saying no to competing demands. Moreover, a public dollar invested in helping to reshore civilian manufacturing is a dollar not spent on something else. All tariffs impose costs — the debate should be whether the costs are worth it, not whether they are free.

Manufacturing is Not a Jobs or Productivity Program

Many political leaders argue that restoring manufacturing creates high-wage jobs or accelerates economic growth. This is rarely the case for several reasons.

Factory jobs no longer pay more than service jobs. Politicians talk about manufacturing jobs as if they’re the backbone of the American middle class. This mostly reflects nostalgia for a time when a man with a unionized factory job could support a family, and own a home, a motorboat, and a cottage on the lake. We should aspire to the abundance and economic security that these memories reflect, without trying to bring back lower paying, mind-numbing assembly-line jobs.1

Growing manufacturing does not create many jobs. Manufacturing now employs only about 8% of the U.S. workforce, so even a miraculous 20% increase in factory jobs would make little difference to overall employment. But we will not see substantial job growth in manufacturing because only highly automated factories can afford to return to the U.S. No American company will hire legions of workers to assemble toasters, polish iPhones, or tighten bolts.

Factories do not increase productivity more than services do. There is a vague popular belief that having more factories increases productivity, but more manufacturing is unlikely to mean greater productivity. Manufacturing often raises productivity in poor countries as they start to industrialize, but it won’t in the United States. If manufacturing improved productivity in advanced economies, both Germany and Japan would be richer than America. They’re not. They would have seen faster economic or productivity growth. They have not.

Manufacturing often adds less value than services. As manufacturing has steadily declined as a share of GDP, the U.S. has outperformed most of the rich world thanks not to factories, but to high-value services such as software, finance, design, logistics, management, and research.

The example of Apple makes this painfully clear. In his indispensable book, Apple in China, Patrick McGee details how the company became more deeply entangled in Chinese manufacturing than any other major American firm. But Apple still captures more than 80% of global smartphone profits while selling only 20% of all units. Apple demonstrates that manufacturing is neither necessary nor sufficient for productivity growth or value capture in a rich economy. McGee capably documents that the problems with Apple’s deep integration with China are not economic – they are geopolitical.

This story is not unusual. Design, marketing, and distribution often account for most of a product’s economic value, especially in brand‑driven and commoditized manufacturing sectors. Manufacturing is still essential, but it is frequently the lowest‑margin, most easily outsourced part of the chain. Modern firms derive the majority of their market value from intangible assets such as brands, design, software, and know‑how rather than from plants and equipment. For companies that operate worldwide, distribution, logistics, and customer support are harder to replicate than basic production.

Crucially, there are exceptions. When production is capital-intensive, technically complex, or protected by process know-how and IP, manufacturing can be a major source of value. Advanced materials, some pharmaceuticals, and semiconductors are leading examples.

Where Manufacturing Matters: Political Power, Spillovers, and General-Purpose Technologies

The strongest case for a strong manufacturing base is geopolitical. Detering adversaries requires precision explosives, modern drones, missiles, and submarines. Consultants and PowerPoint decks won’t do the trick. Large countries like the United States are very unwise to rely on vulnerable overseas producers for critical defense capabilities like semiconductors, drones, ships, and explosives.

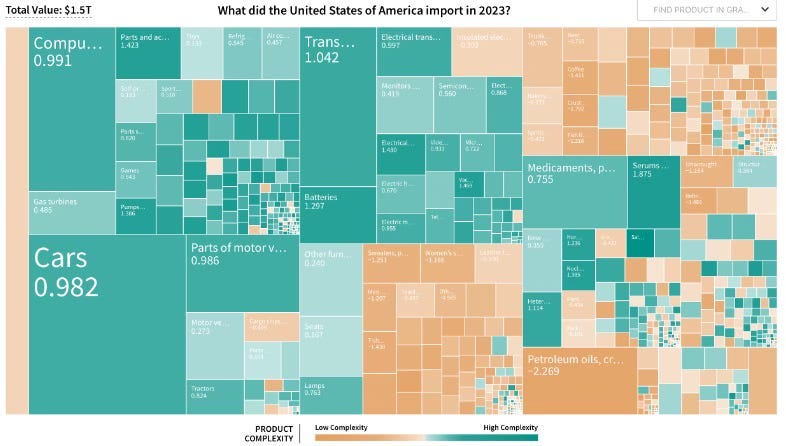

But what of civilian products? Thousands of goods are more complex than socks and T-shirts, yet less complex than semiconductors. The chart below shows total U.S. imports based on their complexity. Clothes, furniture, toys, and other simple, cheap consumer goods are shown in the lightest colors. They make up a surprisingly small share of U.S. imports. On the other hand, we import enormous amounts of stuff shown in green: cars, industrial machinery, electronics, advanced chemicals, pharmaceuticals, metal products, computers, and phones. These are complex, high-value items that are only made in a handful of countries.

Anyone serious about reindustrialization needs a point of view about these goods. Do we need to build domestic capacity to produce them, or is redundant capacity sufficient? Do we need surge capacity for emergencies, or can we depend on reliable allies?

Sorting this out requires that we answer several uncomfortable questions:

Which products are genuine chokepoints that adversaries can weaponize? It has been evident since 2010 that China could use its dominance over rare earths to its strategic advantage.2 China dominates production or processing not only for these metals, but for at least 29 minerals that the U.S. deems critical. In 2024, the U.S. imported 48–76% of its lithium, nickel, and cobalt, all essential for EV batteries and grid storage. China and India supply about 60% of the active pharmaceutical ingredients used in U.S. medicines (and India relies heavily on Chinese inputs.)

Can we shift manufacturing capacity in a crisis? It is easy to mislead ourselves with inspiring WWII-era stories of car factories retooling to produce tanks and planes. Modern weapons and advanced manufacturing are today far more specialized. You can’t turn a Tesla plant into a missile factory as quickly as the U.S. “arsenal of democracy” once turned Ford plants into tank and airplane factories.

How large are the innovation spillover effects from manufacturing? Even when manufacturing itself is not a significant source of value, factory skills sometimes “spill over” into other capabilities. There are three broad categories of spillover effects.

Manufacturing-dependent innovation. In some technically complex industries, like semiconductors or batteries, giving up production means giving up product innovation.3 In these cases, especially in sectors that are essential to national defense, public investment or subsidies can make sense.

Kickstarting manufacturing ecosystems. In other cases, the benefits of innovation are captured not by a single firm, but by a broad ecosystem that is tough to finance privately. Federal CHIPS and Science Act subsidies, combined with New York state incentives, led to Micron’s large memory‑chip complex near Syracuse. The fab was explicitly framed as an “anchor” for a broader regional semiconductor cluster rather than a single plant. Public money supports local suppliers, workforce programs, infrastructure, and tech‑hub grants to deliberately build a supplier ecosystem of tool vendors, materials providers, and specialized service firms around Micron and other chip fabs.

Likewise, the federal Manufacturing Extension Partnership (MEP) network and DOE Industrial Assessment Centers are long‑running examples of public programs that provide technical assistance to small and mid‑sized manufacturers, helping them adopt new processes and connect to higher‑value supply chains.

A range of federal and state initiatives (e.g., Commerce’s Tech Hubs, the Good Jobs Challenge, Recompete, Manufacturing USA institutes, and earlier “Investing in Manufacturing Communities Partnership,”) are designed to strengthen regional ecosystems, not just isolated plants. Examples include Central Indiana’s Heartland BioWorks biomanufacturing hub and other regional advanced‑manufacturing networks where public funds support shared R&D, training pipelines, and supplier‑matchmaking that tie local firms into national and global value chains.

Investing in general-purpose technologies. Historically, many general-purpose technologies have generated large benefits for entire economies well beyond the firms that first developed or adopted them.4 Most rely at some stage on public investment in basic science, mission‑driven programs (especially defense and space), or enabling infrastructure and standards, to reach the scale and maturity needed to transform whole economies. (Today, China may understand these effects more deeply than the United States does.)

Policymakers can make a coherent, efficiency-based argument for public subsidies of general-purpose technologies, especially for advanced research and capital investments in large-scale production. Today, we should ask whether solar, batteries, electric motors, as well as AI and quantum computing technologies are sufficiently critical and the benefits sufficiently diffuse to meet this test.

What is the opportunity cost? Professional talent, skilled labor, electricity, capital, and political attention are all scarce. In a world of finite resources (admittedly not the world the federal government thinks it lives in), money has an opportunity cost. Money spent relocating civilian manufacturing back to the U.S. is money we will not spend on other worthy goals. Plus, we make these decisions in an environment filled with passionate advocates who are far more skilled at articulating the benefits of their policies than the full costs.

Hard Truths About Reindustrialization

I’m broadly sympathetic to the impulse to reindustrialize America. China’s manufacturing dominance is real, and parts of our industrial base, including critical defense needs, are shockingly hollowed out. Every American should care about this.

But sympathy isn’t a plan. Industrial policy is about choosing what to build, what to ignore, what to import, and what to subsidize. In all cases, the U.S. will depend critically on trusted allies who can produce critical goods and sell them to us free of tariffs. Trump has subjected our allies to his dangerous whims, grievances, and tariffs — most recently for opposing his plan to conquer Greenland. Trump explained his need for a ton of tundra as a personal “psychological necessity.”

Trump represents the worst possible form of industrial policy because he cannot distinguish it from self-serving patronage. His personal wealth and family businesses appear to have benefited substantially in the past year from deals that raise serious conflict‑of‑interest concerns, even when they are not clearly illegal. Much of this centers on crypto ventures, international real estate, and licensing deals, as well as regulatory or institutional changes that reduce oversight of such conflicts.5

During Trump’s first year back in office, the U.S. government took equity stakes in companies, bought golden shares, entered pre-purchase agreements, invested in industrial banks, and implemented supply-chain screening. These are state interventions in markets that not long ago would have triggered cardiac arrest among Republicans if Democrats had proposed them. It is hard to know whether the GOP will still favor these things once the Trump fever breaks.

The danger we face is not that America will do nothing. It’s that we’ll do many things badly: scatter subsidies across politically favored industries, oversell job creation, underspecify security goals, tolerate corruption, and underinvest in manufacturing that can genuinely make a sustained difference to American well-being.

Manufacturing does matter – just not in the way most people think. It does not matter everywhere, all at once, at any price. The task isn’t to bring back the past. It’s to decide, with brutal clarity, what elements of our industrial future are actually worth paying for.

Musical Coda

According to the most recent Bureau of Labor Statistics analysis of payroll data, the average seasonally adjusted manufacturing nonsupervisory wage is $29.51/hour, while the private service-providing equivalent is $31.50/hour. As always, averages can mislead: the number of service sector jobs is much higher, so the range of service sector pay is much greater.

China has dominated production of many of the 17 elements known as rare earths since the 1990s because it has lower costs and much more relaxed environmental standards. This became a significant geopolitical problem in the late 2000s and early 2010s, as China began to impose export restrictions and quotas, leading to price spikes and supply shocks. The 2010 Japan-China territorial dispute exposed the world's vulnerability and triggered a global effort to diversify supply chains. This effort failed.

It is also true, as McGee makes clear, that losing production capability to China can enable them to become much more innovative at low-value manufacturing. By investing billions of dollars in training Chinese manufacturing technicians, Apple and Tesla radically accelerated the growth of the Chinese EV industry. This is better news for consumers in Sao Paulo, Bangkok, Florence, and soon Toronto than for workers in Detroit or Fremont.

Classic examples include the steam engine and railroads, which transformed manufacturing, transportation, and urbanization; electric power, which changed factories, consumer goods, and modern communications; internal combustion engines, which reshaped logistics, cities, retail, and tourism; telegraphs, telephones, and radios which reduced communications costs and enabled national markets and mass media; computers and chips that underpin modern software, e-commerce, and digital platforms; and AI, which seems likely to affect a broad range of services, manufacturing, and knowledge work.

Reuters estimates that Trump‑related crypto ventures generated about $800 million for the Trump Organization in just the first half of 2025, far exceeding income from traditional real estate and golf businesses in that period. The Trump family has built new or expanded real‑estate and licensing arrangements in countries such as Qatar and Saudi Arabia, often involving firms with close ties to those governments. Trump’s net worth has reportedly doubled since returning to office, with analyses crediting real‑estate deals and, especially, crypto‑linked assets, along with the new monetization of his political and religious brand (for example, Bible sales generating millions in fees in 2025).

Just so smart. Spot on.