Waste in China is Lovely But Costly

In 2026, China overproduces while America underinvests.

Returning from China risks whiplash. It is jarring to leave the land of gleaming cars, abundant housing, new roads, spectacular greenways, and spotless bridges, tunnels, train stations, and airports, and arrive in a city known for its $1.7 million public toilet.

I Thought Capitalists Overproduced and Communists Starved?

It was not supposed to turn out this way. Because we encourage investors to independently bet on the same opportunity, we expect competitive capitalism to produce large surpluses. Each investor wants to strike it rich, but coordination is impossible, and optimism is cheap, so we get railway manias, dot-com or fiber-optic gluts, and too many car or steel companies. The all-American result is overcapacity, which wastes capital and causes companies to fail, but leaves society with lower prices, fewer weak players, and lots of shiny new infrastructure.

Communist state planning, on the other hand, tries to avoid this waste by matching production to social need. But central planners can’t really foresee demand – they only see plan targets – so shortages of things people actually want typically coexist with warehouses full of things they don’t.

So how exactly did China end up looking more like the 19th-century American railroad boom than like Gosplan, while outside the AI frenzy, the U.S. and Europe look more like cautious, return-on-capital-obsessed late-stage firms than the industrial dynamos of our recent past?

China Has Overbuilt. A Lot.

Understanding overcapacity in China requires separating industrial overcapacity (factories that make too much stuff) from infrastructure/real estate overinvestment (local governments that build things that nobody uses).

Housing. The most visible sign of this when you visit China is “ghost towns” or “ghost hotels”. This is not a minor problem. China has about 65 million empty houses – enough to house the entire population of France. This is about 20-30% more residential floor space than China’s (shrinking) population needs.

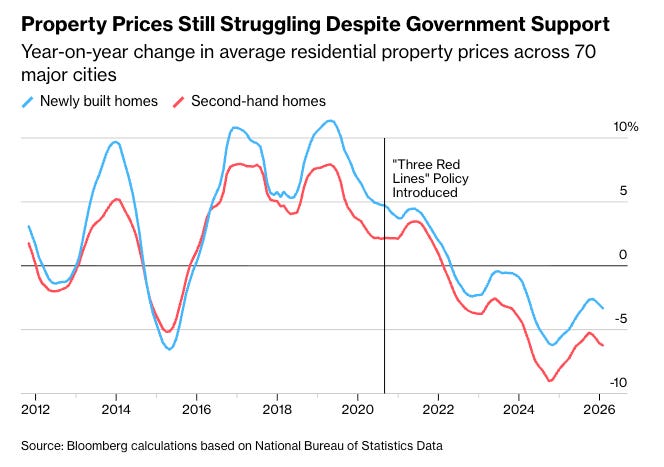

In contrast, the U.S. needs more housing. We could use 5-10 million more homes to meet demand, mainly in our most productive cities. Although housing remains tight in Tier-1 cities like Beijing and Shanghai, vacancy rates in Tier-3 or 4 Chinese cities often exceed 30%. As noted previously, this has led China to relax its hukou system, which controls who can migrate from the countryside to new cities.

Factories. China has massively overbuilt factories as well. China’s “New Three” (EVs, lithium batteries, and solar) are the current focus of global trade tensions. China’s total vehicle production capacity is nearly 50 million vehicles/year. Domestic demand sits closer to 25-27 million, so China is flooding the world with low-cost cars and slashing prices. North American auto and steelworkers are not amused, although U.S. consumers will soon lust after the low-cost, high-quality EVs being driven by our Canadian and Mexican neighbors. These cars are effectively banned in the U.S. (unless they are rebadged as Volvos or Polestars.)

Infrastructure. Finally, China’s public transportation infrastructure is impressive, but it is a combination of highly efficient hubs and vastly underused regional projects. The Chinese have become at least as good at building ”Bridges to Nowhere” as the U.S. has. Specifically:

Airports. China has built more than 270 airports, but 41 of these handle 84% of all passengers. The vast majority lose money.

Trains. At least a quarter of all high-speed rail stations are overbuilt and run only a handful of trains each day. High-speed rail debt in China is almost a trillion dollars.

Bridges and tunnels. In very poor rural provinces like Guizhou, many world-class bridges serve low-traffic rural roads, leading to a debt-to-GDP ratio in that province exceeding 150%. (It is also possible that without bridges and tunnels that lessen Guizhou’s isolation, the province can never catch up to the rest of China.)

What does wasted infrastructure spending actually cost the average Chinese citizen? It represents a drag on economic growth that can show up as high youth unemployment, widening income disparities, and lower living standards.

Economists measure capital-output ratios, which indicate how much growth an economy generates per unit of investment. In the 2000s, China could get a unit of growth by investing three units of capital. Today, they need to invest more than 9, meaning China now has to spend three times as much to achieve the same level of economic growth as it did 20 years ago. These diminishing returns reflect the ultimate “cost” of overcapacity.

You can also measure the debt that China has used to finance public infrastructure. The money is typically borrowed by so-called Local Government Financing Vehicles – the “hidden” companies that governments use to build roads and bridges. Fitch estimates that these LGFVs face a $4.7 trillion debt-service gap. The interest paid on the “Special Purpose Bonds’ used for infrastructure now accounts for 10% of local government budgets.1

How Did This Happen?

To understand the paradox of a state-planned economy overproducing while the headquarters of global capitalism underproduces, we need to ask who bears the downside of overinvestment. And whose interest does the financial system serve?

In China, local governments, state banks, and SOEs can absorb enormous losses because the political and economic system doesn’t force them to mark losses to market or answer to shareholders.2 Near term, waste costs less in China.

Still, a Chinese municipality can build a metro that won’t break even for forty years; a U.S. transit authority facing the same math can’t get it funded. This isn’t planning defeating markets — it’s a system with a very high tolerance for sunk capital costs outcompeting one with a very low tolerance.

Second, ask: whose interests does the financial system serve? Post-1980s, Western capitalism reorganized itself around shareholder returns, share buybacks, and asset-light business models. Capital became disciplined in a specific way: far more allergic to long-duration, low-return physical investments.

Housing underproduction in the U.S. and UK, for instance, isn’t really a failure of markets in the abstract — it’s the predictable output of a system where incumbent homeowners are voters, zoning is local, and developer capital demands quick returns. China’s system has the opposite distortions: developers overbuild because land sales fund local governments, housing is the main vehicle for household savings, and buyers pay for a house before it is built. And there is no legal infrastructure that enables incumbent homeowners to fight new development.

So the paradox is less markets vs state planning than the kind of overcapacity that capitalism generates in its competitive, industrial phase. Once economies mature into a rentier-friendly, financialized form, they lose the overcapacity-generating property that had once defined them. (Of course, the current AI investment frenzy may refute this theory. We’ll know soon enough.)

China, meanwhile, built a hybrid system that preserves the “throw capital at physical stuff until it’s cheap” logic of early industrial capitalism but funds it through state-directed credit rather than equity markets. It’s not that Chinese planning beat Western markets; it’s that early-stage state-backed investment “out-capitalism’d” mature Western capitalism.3

It may be shiny for the moment, but overcapacity in China is expensive and economically destructive. Ghost cities, Evergrande-style property collapses, and the current deflationary pressures suggest that overcapacity in China can be just as catastrophic as its Western counterpart has been. The question isn’t whether the losses happen but whether the system that generates them also generates the productive residue — the cheap solar panels, the high-speed rail network, the battery supply chain — that justifies the waste ex post. That too is still an open question.

ICYMI

The health benefits of owning a dog are statistically nontrivial.

Mr. Beast now has 469 million YouTube subscribers — more than the U.S. population.

Half of Americans would abolish ICE.

Brussels is so awash in cocaine that it worries about social stability.

Switzerland amends its constitution to require businesses to accept cash.

Stablecoins are now massive holders of U.S. debt. No, not good.

In 2025, the EU produced more energy with renewables than with fossil fuels.

China is managing a major shift in local government financing from land concession taxes to a more diversified set of revenues. They are slowing infrastructure spending and swapping local for federal debt.

The details are complex, but the local financial burden remains acute. The central government’s ongoing CNY 10 trillion debt-substitution program—which refinances hidden LGFV debt into explicit local government bonds—is designed to address the large debt-servicing gap. However, Fitch notes that it currently covers only about 30% of that gap.

To be clear, nonperforming loans are bad loans, whether or not a state-owned bank acknowledges them. The bank has less capital and is weaker than it would be if it had backed more productive economic activity, whether it formally admits it or not.